What It Really Costs to Own a Home in Denver Right Now (June 2026)

What It Really Costs to Own a Home in Denver Right Now (June 2026)

If you've been watching mortgage rates this week, you noticed they nudged back up. The 30-year fixed averaged about 6.52% in Freddie Mac's latest weekly survey, up slightly from the week before, with daily trackers showing roughly 6.6% mid-week. The reason isn't local at all: rates have drifted higher since the start of the U.S. conflict with Iran, which has pushed oil prices up and reignited inflation concerns. When inflation worries rise, mortgage rates tend to follow.

But here's what I tell every Denver buyer and seller I work with: the headline rate is only one line on the page. The bigger story in 2026 is the full cost of owning a home here, and two of the three biggest pieces — insurance and property taxes — are the ones people most often forget to plan for. Let's break down what owning a Denver-area home actually costs right now, and what it means whether you're buying, selling, or simply staying put.

Mortgage rates: steady in the mid-6s, with some weekly noise

After dipping earlier this spring, rates have settled into the mid-6% range and have been holding there for several weeks. Most housing economists expect them to stay above 6% through the rest of the year, with no dramatic swings unless the broader economic picture shifts.

What does that mean in real dollars? On a $480,000 loan (roughly a 20% down payment on a $600,000 home) at today's rate, you're looking at about $3,050 a month in principal and interest. On a $400,000 loan, closer to $2,550. Those are the numbers that show up on most online calculators — and they're only part of your real monthly payment.

The insurance squeeze most buyers underestimate

This is the cost that catches people off guard, and it's become one of the most-searched homeowner questions in Colorado for good reason. The average homeowners insurance premium in Colorado is now around $4,100 a year — a roughly 137% increase over the past decade, according to figures cited by the National Bureau of Economic Research. Our state's hail and wildfire exposure is the driving force, and it's a year-round risk rather than a seasonal one.

A few things worth knowing:

- It's not just single-family homes. Many condo and townhome associations have seen their master policy premiums jump, and some have passed special assessments along to owners. If you're shopping condos in neighborhoods like Capitol Hill, Baker, or Cherry Creek, the HOA's insurance situation is now a core due-diligence question.

- Quote insurance before you make an offer, not after. A 20-minute call to an insurance agent before you go under contract can prevent a nasty surprise two weeks before closing. I help my clients build this into their search from day one.

For a $600,000 home, that $4,100 annual premium adds roughly $340 to your monthly payment — money that doesn't show up on a generic mortgage calculator.

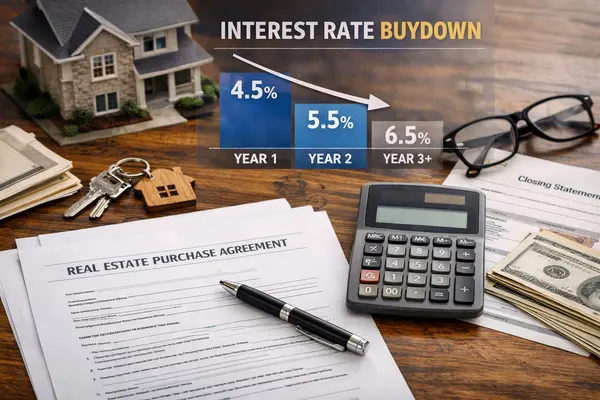

Property taxes in 2026: why your bill may be higher even if your home's value didn't move

Colorado reappraises property every two years, and the most recent cycle showed values across the metro staying relatively flat — some counties slightly up, some slightly down. So you'd expect tax bills to hold steady. Many didn't.

The reason is structural. A temporary $55,000 reduction to taxable value, in place for the prior two years, expired — so even a home whose market value stayed flat effectively had $55,000 added back to its taxable value. On top of that, a change in school-district assessment rates lifted the tax base further. The City and County of Denver held its mill levy flat for 2026, but the combination of those state-level changes still pushed many bills up.

The takeaway for buyers: don't trust the old tax estimate on a listing portal. Those figures are often a year or two behind, and the gap can be $200–$400 a month on your real payment. When you're getting pre-approved, ask your lender to run your numbers using the current-year tax figure for the specific property, not last year's.

The new affordability math for Denver buyers

Put it all together and you get a clearer picture of why "the rate" is a misleading shorthand. On that same $600,000 home, your real monthly cost looks more like:

- Principal and interest: ~$3,050

- Homeowners insurance: ~$340

- Property taxes: varies by district, often $400–$600

- HOA or metro district fees (if applicable): varies

The encouraging news is that the market itself has shifted in buyers' favor. The latest Colorado Association of REALTORS report shows pending sales rising even as new listings stay light — a sign of a more balanced, sustainable market heading into summer. Inventory across the metro is meaningfully higher than a year ago, which means more time to compare homes, more room to negotiate repairs and concessions, and far less pressure to waive contingencies than buyers faced in 2021–2023.

My advice: build your budget around the all-in monthly payment, not just principal and interest. If you do that homework up front, the current market gives you real leverage to find the right home at the right number.

What this means for sellers

If you're selling, rising ownership costs are quietly shaping how buyers shop. Many are adjusting their price range to absorb higher insurance and taxes, which means pricing accurately from day one matters more than ever. Recent metro data puts the median closed price in the low-to-mid $600,000s, and well-prepared, correctly priced homes are still attracting strong activity — while overpriced listings sit. The homes winning right now share three traits: smart pricing, strong presentation, and professional marketing.

The bottom line

Mortgage rates grabbed the headlines this week, but the fuller story in Denver is that the true cost of owning a home is being shaped just as much by insurance and taxes. The buyers and sellers who plan around the complete picture — not just the rate — are the ones making confident, well-timed decisions in this market.

If you'd like a clear, personalized breakdown of what a specific home would actually cost you each month — rate, taxes, insurance, and all — I'm always happy to run the numbers with you. That clarity is often the difference between a stressful purchase and a smart one.

— Jordan Jordan Wagner | Denver-Area Real Estate jordan@jordanwagnerrealtor.com

Categories

Recent Posts

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "